Sorry, we couldn’t find the page you requested Financial Contact Authority

Contents

For all financial assets measured at amortised cost or at fair value through other comprehensive income , lease receivables and contract assets, a loss allowance is recognised representing expected credit losses on the financial instruments. Under US GAAP, no expenses incurred on internally generated goodwill may be capitalized. Typical items expensed include internally generated brands, mastheads, etc., startup costs, training costs, advertising and promotion, relocation costs, etc. When intangible assets are acquired when another company is acquired, they are capitalized separately from goodwill if they arise from contractual rights , other legal rights , or have the ability to be separated and sold . Accounting standards require discontinued operations to be presented separately in the financial statements. This allows a realistic and fair assessment of the company’s future financial results.

The material uncertainty created by COVID-19 is especially relevant to the valuation of Land and Buildings, and further information is available about the estimated valuations in note 7. Annual report of the consolidated financial cometcoin results of the Scottish Government, its Executive Agencies and the Crown Office, prepared in accordance with International Financial Reporting Standards . The Audit Scotland report on the accounts is also linked and is unqualified.

Resources and accruing resources may be used only for the purposes specified and up to the amounts specified in the Budget Act. The Act also specifies an overall cash authorisation to operate for the financial year. The Scottish Government is not, therefore, exposed to significant liquidity risks.

Why is goodwill important to accountants and financial modellers?

Where output tax is charged or input VAT is recoverable, the amounts are stated net of VAT. The road network is valued at depreciated replacement cost as it is deemed to be specialist in nature. The road pavement element is valued using agreed rates determined to identify the gross replacement cost of applicable types of road on the basis of new construction on a greenfield site. These rates are re-valued annually using indices to reflect current prices and are also updated when new construction costs become available as comparators to the costs previously identified for specific road types. To understand what is meant by the impairment of assets in a little more depth, let’s see an example.

Its primary objective is to provide cost-effective risk pooling and claims management arrangements for Scotland’s NHS Health Boards and Special Health Boards. Funds received from the European Union , are treated as income and shown in the relevant Portfolio Outturn Statement. Expenditure in respect of grants or subsidy claims is recorded in the period that the underlying event or activity giving entitlement to the grant or subsidy claim occurs. Any related payable or receivable balances are reflected in the Statement of Financial https://cryptolisting.org/ Position. Where there is a unitary payment stream that includes infrastructure and service elements that cannot be separated, the various elements will be separated using estimation techniques including obtaining information from the operator or using the fair value approach. Financial guarantee contract require the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the original or modified terms of a debt instrument.

At 1 July 1999, the right to the sums outstanding was transferred to the Scottish Ministers who must pay the repayments and interest to the Secretary of State for Scotland via the Scottish Consolidated Fund. The loans to Scottish Enterprise and Scottish Homes have since been repaid. This implementation date for IFRS 17 is not yet confirmed and the impact has not yet been determined. The Financial Reporting Advisory Board are considering implementation of the standard in the public sector.

This also means that the Scottish Government is now the funder of last resort in cases where the developers/owners cannot meet their decommissioning obligations. As the size of the Scottish portfolio of offshore energy projects grow so does the cumulative value of the decommissioning obligations and contingent liability. The Scottish Government occupies a number of leased properties which have dilapidations clauses in the leases. These properties are maintained in excellent order, but there is a potential liability to reinstate the internal layout of these buildings to their original floor plans.

14 European Union Funds

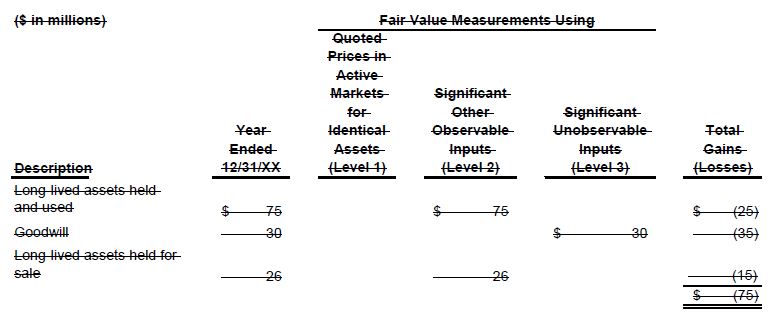

The following assets have been presented for sale by the Scottish Government. Assets classified as held for sale are measured at the lower of their carrying amount immediately prior to their classification as held for sale and their fair value less costs to sell. Additional pension liabilities arising from early retirements are not funded by the scheme except where the retirement is due to ill health.

These acquisition costs are reported as expenses in the statement of profit or loss and not included in the calculation of goodwill. In accounting terms, this extra value is known as ‘goodwill’ and it is considered an intangible asset. The concept of goodwill takes on particular importance when a company is looking to acquire another company. Often, they will need to be willing to pay a price premium over the market value of the company, particularly when that valuation is based simply on the net assets.

The revaluation model

A financial instrument is a contract that gives rise to a financial asset of one entity or financial liability or equity investment of another entity. Examples of financial assets include investments in stocks or bonds of another company. Some assets, such as derivatives, may be classified as either a financial asset or a liability depending on their value. Subsequent to initial recognition, a financial asset is carried either at fair value or amortized cost. In case of an intangible asset with an indefinite useful life, a company records no amortization but reviews the assumption of indefinite life and any impairment at least annually. While some analysts assign zero value to all intangible assets, a better approach to look at each individual asset.

The post-tax profit/loss of the discontinued operations is added to any post-tax gain/loss on disposal. Separately, a break-up of the two amounts should be included either on the face of the income statement or in the notes to the financial statements. This material valuation uncertainty applied not only to the valuation of the Scottish Government portfolio properties, but also to properties held by the individual Agencies within the consolidation boundary and properties within NHS Trusts. Of the NHS Trust and Scottish Prison Service assets that the material valuation uncertainty applies to, significant proportions relate to specialised assets valued on a depreciated replacement cost basis. Specialised operational assets are valued on a modified replacement cost basis to take account of modern substitute building materials and locality factors only.

At the end of the contract period the building will revert to NHS ownership. The Scottish Government has instituted funding advances for certain EU CAP payments. Following EU Exit, Euro denominations were sold once EU funding was received. As at 31 March the year end balance of £95.5m is the sterling equivalent of €106.9m. Labour Force Survey data – to convert income percentiles to cash amounts, regarded as more reliable than cash values from BHPS due to large sample sizes. British Household Panel Survey data – used for derivation of earnings and employment models and income distributions, especially later career stage earnings and steady state models.

- NPD/PPP/PFI transactions are accounted for in accordance with IFRIC 12, Service Concession Arrangements which sets out how NPD/PPP/PFI transactions are to be accounted for in the private sector.

- The Scottish Government has material transactions with local government bodies, Regional Transport Partnerships, Community Justice Authorities and Scottish Water.

- Property, plant and equipment is initially measured at its cost, subsequently measured either using a cost or revaluation model, and depreciated so that its depreciable amount is allocated on a systematic basis over its useful life.

- NHS Fife hold 2 FPI contracts, which are both held as non-current assets of NHS Fife Board and the liabilities to pay for the properties are accounted for as finance lease obligations.

- Historical cost includes all costs incurred in making an asset operable and may include purchase price, delivery costs, installation costs, etc.

- Stirling Health and Care Village – Service concession for the development and right of use of Community Health and Care facilities which brings together on one site a range of health, local authority and other partner organisation’s services.

Mid-market rent is a type of affordable housing where rents are lower than in the private market, but higher than social housing. Scottish Health Innovations Ltd is a company that works in partnership with NHS Scotland to protect and develop healthcare innovations. The company is limited by guarantee with three members, the Scottish Ministers, the National Waiting Times Centre, and NHS Tayside. In December 2019 the Ferguson Marine shipyard was brought into public ownership.

History of IAS 16

Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less an estimate of likely impairment. Impairment of trade receivables is calculated through an expected credit loss model. The Scottish Government reports segmental information within its outturn statements which are prepared on the basis of Ministerial portfolios. Operating income is income that relates directly to the operating activities of the Scottish Government. It includes fees and charges for services provided, on a full cost basis, to external customers, public repayment work and income from investments. It includes both income applied with limit as outlined by the Scottish Budget documents and income not applied.

IAS 34 — Interaction with IAS 36 and IAS 39

Credit risk is the risk that a third party will default on its obligations. The maximum exposure to credit risk at the balance sheet date in relation to each class of financial asset is the carrying amount of those assets net of any impairment. The StEP model uses information from two sub-models, an earnings model and a repayments model, to predict outcomes for student borrowers.

Non-current assets are assets other than those which meet the criteria for classification as current assets. Typical non-current assets include property, plant, and equipment , investment property, intangible assets, goodwill, financial assets, and deferred tax assets. The objective of IAS 16 is to prescribe the accounting treatment for property, plant, and equipment. The principal issues are the recognition of assets, the determination of their carrying amounts, and the depreciation charges and impairment losses to be recognised in relation to them.

According to standard accounting rules, also known as the Generally Accepted Accounting Principles , as goodwill is an intangible asset it is only recorded when there is a sale of the entire business or a subsidiary of the business; it cannot be generated internally. It can only be recorded in the accounts when there is an actual amount that has been paid over the fair price of the company. However, a calculation or estimate of the goodwill is often made during negotiations. IFRS and US GAAP both require measuring assets held for sale at the lower of the carrying amount and fair value less costs to sell. The hospital services are provided under a contract between Lanarkshire Health Board and Prospect Healthcare Limited, with hard and soft facilities management services being supplied under a subcontract to ISS Mediclean Limited. Mid Argyll Community Hospital and Integrated Care Centre Lochgilphead – NHS Highland financed the development of the Mid Argyll Community Hospital and Integrated Care Centre in Lochgilphead.

Virtual Consultation

Many of our patients come to us from across the country and around the world. For your convenience, we are pleased to offer a “Virtual Consultation” with our doctors. To begin the process, click on the link below. Please be prepared to supply us with some basic information as well as photographs to help our doctors answer your questions and recommend a course of treatment.

Home | Contact Us | Consultation | Transplant Pricing | Procedures | The Results | Men's Gallery | Women's Gallery | Testimonials | Sitemap | Privacy Policy

FREE Hair Transplant Guide

This Free guide arms the “Novice” to navigate an unregulated industry. Written by Daniel J. Wagner, a prominent Hair Transplant insider and CEO. Learn “How To” get the natural looking results you deserve the first time. Learn the “Questions” first time patients should be asking but don’t... Read More

Call for a free consultation